The rally in the US markets may soon lose its fizz.

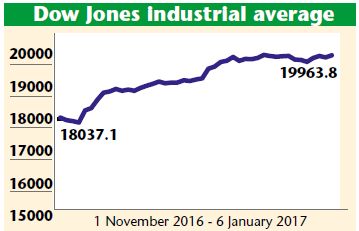

The US markets are on a roll since Donald Trump won the US Presidential elections in November 2016. This is in sharp contrast to the sentiments prevailing during the pre-election time, when everyone was expecting a sharp correction in the event of Trump’s victory. Since the first week of November 2016, Dow Jones Industrial Average (DJIA) has shot up by 11.8 per cent to 19999.63, missing the ‘20000’ milestone just by a whisker. US equities have seen inflows of nearly $70 billion since 8 November 2016. During the same period, NIFTY 50 has corrected from 8600 levels to 8200 levels, after hitting 7900 levels just before Christmas.

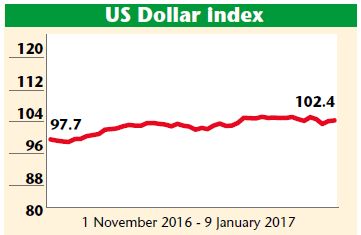

Trump’s victory has created a huge ripple effect in the financial markets, with the Dollar Index strengthening from 97 to 103 in the past two months. The 10-year US bond yields have gone up from 1.78 per cent on 4 November 2016 to 2.42 per cent on 8 January 2017, after hitting highs of 2.64 per cent on 15 December 2016. These developments have resulted in massive sell-off from EMs including India. The interest rates in India have been softening – especially post-demonetisation.

Since November 2016, India has seen a huge outflow of hot money from debt as well as equity markets, as the spread between Indian bond yields and the US bond yields have narrowed from over 500 bps earlier to just under 400 bps now. This sharp rally in the Dollar Index and strengthening of US bond yields after Trump’s victory is expected to fizz out soon, as investors come to terms with reality. Lots of positives are already factored in after the sharp rally in the US markets. The stronger dollar in the longer run would affect the country’s growth prospects, especially at a time when other countries are in a rush to depreciate their currencies.

The recovery of the US economy is expected to be more gradual and not ‘V’ shaped as is reflected from the current state of the markets. The excesses built into the US markets will start fizzing out as early as 20 January, when Donald Trump is sworn in as the 45th President of the US.

As the rally in US bond yields and Dollar Index subside, foreign investors will once again start looking at ’emerging markets’ like India, which is in the process of building a strong base for the next phase of growth. Pressure on the Indian markets is now expected to start easing. The impact of the demonetisation-led slowdown should remain short-lived. According to the SBI report, 67 per cent of the demonetised currency will get replaced by the end of January 2017 and 80-89 per cent by the end of February 2017, if the central bank keeps printing notes at the current pace. If this was to happen the Indian economy could witness a ‘V’ shaped recovery. The cash crunch has already started easing and the demand is slowly coming back to normalcy.

The Indian equities, which have corrected since November 2016, may buck the trend and move up to catch up with the ongoing global rally. The undercurrent in the global equities is extremely strong. Since November 2016, FIIs have pulled out $5.7 billion and $4.2 billion from Indian bond and equity markets respectively. In sharp contrast, long-term investments in the form of FDIs have increased by 27 per cent to $27.8 billion during April-October 2016, suggesting that India continues to remain an attractive investment destination from a long-term perspective. FIIs have remained net buyers in Indian equities in 15 out of the 17 calendar years since 2000. The current underperformance in Indian equities may not last for long. It is just a matter of time before hot money will again start flowing back into Indian equities. However, in the near term, uncertainties over the budget announcements and the election results in five states will continue to weigh on the market sentiments

This article was originally published in Business India Magazine.

Write to us at news@valuelineadvisors.com

Disclaimer: The views expressed in this article are personal and the author is not responsible in any manner for the use which might be made of the above information. None of the contents make any recommendation to buy, sell or hold any security and should not be construed as offering investment advice.