Weakness in the dollar index to drive rally in Indian equities.

Indian equities are interestingly poised. On the one hand, the Narendra Modi led BJP has won the elections with a larger majority, thereby providing political stability and has laid a strong foundation for a strong economic growth in the years to come. On the other hand, the Indian economy is undergoing tremendous turbulence, as is visible from the ongoing slowdown and tight liquidity conditions. The problems faced by the Indian economy are severe and will take a long time to resolve, as is highlighted herein.

There is a severe slowdown in consumption demand, driven by stress in rural economy. The farm crisis and delayed monsoon has been a cause of concern for the sector and the economy as a whole. The auto sector, which contributes 7 per cent to the country’s GDP, is also in the doldrums. India’s financial sector is undergoing tremendous stress, driven by liquidity crisis in NBFCs and the banking system. Even though the RBI has been infusing liquidity into the system, the quantum of liquidity needed is extremely high.

The delay in the onset of monsoon has been a major cause of concern for the economy. However, after the initial dry spell in June, monsoon has eventually picked up in the first week of July – turning the deficit of June into an overall surplus in certain parts of the country. This should help in reducing rural stress.

Despite a stronger mandate to the Modi government, Indian equities have failed to rejoice due to severe headwinds faced by the economy. The tight liquidity conditions, along with the failure of corporate earnings to revive, have affected the market sentiments. At present, even if NIFTY 50 is holding on steadily, the broader markets are clearly struggling to stay afloat. The midcaps and small caps have been beaten out of shape. A majority of the BSE 500 stocks are trading below their 200 DMA.

The ongoing liquidity crisis has resulted in multiple defaults in renowned corporate groups such as Jet Airways, Zee, DHFL, Cox & Kings, IL&FS and Reliance ADAG gorup, as also many others. This crisis situation looks far from being resolved in the near future.

The investors are now awaiting the Union budget announcement by the new finance minister Nirmala Sitharaman on 5 July 2019. The markets are anticipating some strong fiscal stimulus – even if it leads to fiscal slippages in the near term. Any announcement directed at the resolution of the liquidity crisis and reforms directed at reducing rural stress should help the markets gain some confidence. Currently, despite lower government bond yields, lending rates have remained high. Improvement in liquidity conditions will help in better transmission of interest rates in the economy.

In March, the US Federal Reserve had indicated the reversal of its stance of monetary tightening. With signs of slowdown and lower-than-expected inflation rate in the US, the Federal Reserve could announce a fresh round of easing as early as next month. Similarly, ECB too has adopted a more dovish tone. These events have led to rising gold prices. Gold prices have touched a six-year high, surging 12 per cent during the month. The geo-political tensions between US and Iran have further supported rise in gold prices.

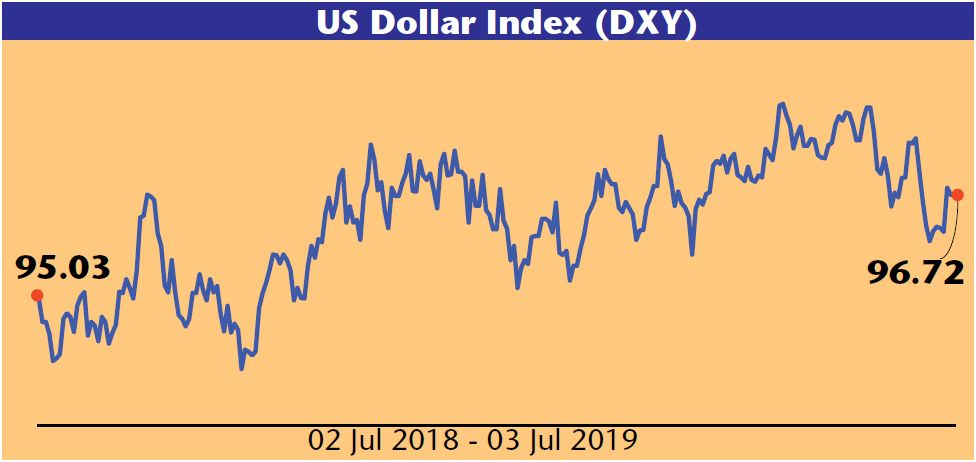

The dollar has started weakening, as is reflected from the fall in Dollar Index (DXY), which is an index of the value of dollar relative to a basket of foreign currencies. The DXY has fallen to about 96 levels and is expected to extend its downward momentum with further weakness in the US economy. The fall in DXY provides a boost to the Indian equities, as it results in a flow of foreign money. Amidst the ongoing liquidity crisis, India’s only hope is the foreign flows into the Indian equities, once Fed reverses its stance to easing.

The crude, which was rising on the back of production cuts by OPEC, has started falling due to an anticipated slowdown in developed economies. The fall in crude prices should be beneficial for India. These factors, coupled with the Fed’s monetary easing, should propel Indian equities to new highs in the second half of 2019. While NIFTY 50 looks expensive on a P/E basis, the market-cap to GDP ratio for Indian equities is just about 80 per cent, suggesting inexpensive valuations of Indian equities. The ongoing under-performance in equities is creating a strong base for out performance of Indian equities in the second half of 2019.

This article to be originally published in Business India Magazine.

Write to us at news@valuelineadvisors.com

Disclaimer: The views expressed in this article are personal and the author is not responsible in any manner for the use which might be made of the above information. None of the contents make any recommendation to buy, sell or hold any security and should not be construed as offering investment advice.