The US China trade dispute is likely to be settled soon.

As mentioned before in our guest column (Column, Business India, 28 January), Indian markets are expected to eventually catch up with the ongoing global emerging market rally, which started in early 2019. Indian equities have finally managed to reverse the downtrend and have seen a sharp rally since mid-February. They were lagging primarily due to the political uncertainty pertaining to the impending elections, due in April-May 2019.

The turnout of events after the terrorist attack in Pulwama (Jammu & Kashmir) on 14 February and the strong retaliatory action by the Indian Air Force through its air-strikes on terrorist camps in Balakot (Pakistan) have drastically improved the odds in favour of the ruling government winning the elections. These events also have changed sentiment and reversed the trend of Indian markets.

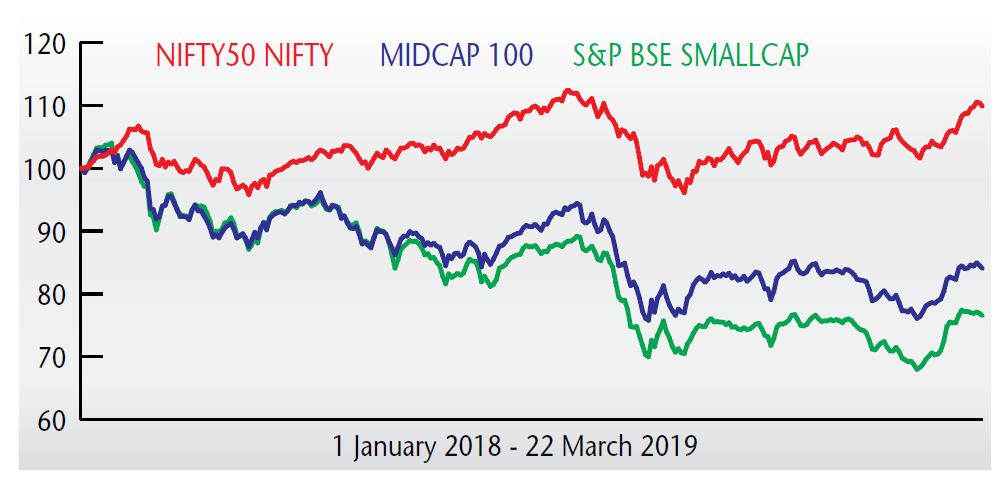

Earlier, while NIFTY50 kept holding on, broader markets were clearly under pressure, with mid-cap and small cap stocks continuing to hit lows. Since end February 2019, there has been a broad-based and sharp recovery in the Indian markets. The sharp rally has resulted in an explosive swing in the market breadth from over-sold to over-bought levels in a short time.

Small-cap and mid-cap stocks have made a strong come-back since then. BSE Small-Cap and NSE Mid-Cap 100 Indices have been up 12.5 and 10.4 per cent respectively since 18 February, as against a 7.7 per cent rise in NIFTY50. A large number of Indian stocks have shown a break-out in the trend, reflecting the strong bullish bias.

Recently, the US Fed Reserve turned dovish and announced a pause in the interest rate hike for years 2019 and 2020, signalling an end to the ongoing tightening cycle. This sudden announcement has triggered fear of a slowdown in the US economy, resulting in a sharp correction in 10Y US treasury yields, which fell below the three-month treasury bill yields, resulting in an inversion in the yield curve. This reflects the fact that investors are factoring in interest rate cut, going forward.

From an emerging market perspective, this development has mixed signals. The end of a tightening cycle and the eventual cut in interest rates by Fed (as is reflected from the inverted yield curve) could result in a rush of liquidity into emerging markets. It also reflects the possibility of a slowdown in the US economy.

The inverted yield curve could also possibly be the outcome of the ongoing US-China trade war. As it gets resolved, the yield curve is expected to correct itself.

The 10Y US bond yields are at 2.44 per cent, while the 10Y GoI bond yields stay at 7.32 per cent. The yield differential stands at 4.88 per cent, as against the inflation differentials of just about 1-2 per cent. The real interest rates in India are among the highest globally. India is already seeing a rush of foreign liquidity and appreciating currency and this trend is now expected to gain strength. The Indian rupee is now among the best performing currencies globally.

The Indian economy is currently facing a tight liquidity condition. Higher real interest rate provides significant head room for the RBI to cut interest rates and infuse liquidity to support economic growth.

Indian economy is all set to move north as the negative impact of multiple shocks – demonetisation, as also the hiccups from the roll-out of GST, high crude prices, RERA, etc – are already behind. Also, the government’s thrust on spending on infrastructure development is expected to yield results. The announcement of direct cash transfer to the farmers and tax benefits to the middle class should boost demand in the economy.

The Insolvency & Bankruptcy Code (IBC) has been instrumental to a great extent in tackling the NPA crisis in the Indian banking system. It has helped in the recovery of bad loans from large accounts. These steps have started creating fear in the minds of rogue promoters, who preferred to willfully default on repayment of loans.

India’s macros are clearly showing signs of improvement, with stability in crude prices, steady inflation and appreciating currency. A stable political environment post elections should help boost investor confidence in India.

After over a year-long downtrend, Indian equities are now poised for a much larger rally. The recent run-up is just the beginning and the rally is expected to gather steam once a stable government is in place. Indian equities are clearly starring in one of the most furious bull runs in history. This ought to be the mother of all bull runs.

This article was originally published in Business India Magazine.

Write to us at news@valuelineadvisors.com

Disclaimer: The views expressed in this article are personal and the author is not responsible in any manner for the use which might be made of the above information. None of the contents make any recommendation to buy, sell or hold any security and should not be construed as offering investment advice.