Slew of measures by the government provides ray of hope for the markets

The Indian economy has been witnessing tremendous turbulence with slowing economic activities across major sectors. The GDP growth rate has hit a five-year low at 5.8 per cent in 4Q-FY19. The liquidity crunch in the run up to elections has continued even after the formation of the new government. Defaults by large corporates such as IL&FS, Jet Airways, Cox and Kings, Essel group, DHFL, Manpasand Beverages, among others have worsened the liquidity situation.

There is no serious lending happening in the economy as lenders turn risk averse. NBFCs are struggling with a cash crunch due to an asset-liability mismatch amid the ongoing economic slowdown. Banks too are hesitant to lend as NPAs continue to haunt them. The government is fixing the systemic issues with a stick in hand. The clean-up is happening at an unprecedented pace with zero tolerance for systemic inefficiencies. This is affecting the functioning of the businesses.

The auto sector is undergoing one of the worst slowdowns ever, with negative volume growth for past many months. The lack of auto demand is resulting in OEMs cutting down production and rationalising inventories across the supply chain, leading to lay-offs in the industry. Auto sector contributes about 7.5 per cent to India’s GDP and a whopping 49 per cent of India’s manufacturing GDP with a large economic multiplier impact. The leading FMCG companies too have been complaining about slowdown and job cuts.

Even on the global front, things are not rosy. The inverted yield curve and falling yields indicate clear signs of economic slowdown with possibility of recession. In the first of its kind, the Danish Bank recently launched the world’s first negative interest rate mortgage. The US-China trade war is affecting global growth prospects.

These factors have a direct bearing on the performance of equities. In India the bear phase started about 18 months back when the government introduced long-term capital gains tax on equities in the budget. This phase has done enormous damage to investors’ wealth across the board. The damage is not so much apparent from performance of NIFTY50. However, if one removes the top 10 best performing stocks from NIFTY50, the balance NIFTY40 is quoting at an equivalent of NIFTY 9000 levels.

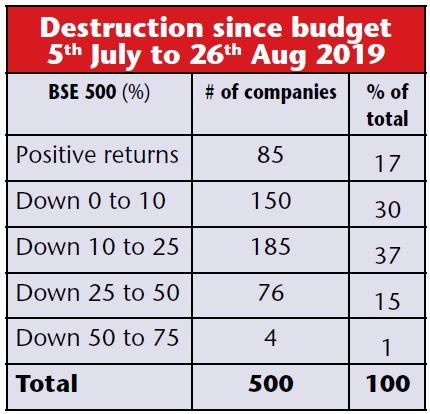

In general, the budget announced in July 2019 was not bad, but for the few provisions which directly affected FIIs. In an attempt to boost revenues, the new finance minister announced higher surcharge on super rich individuals and AOPs, which included non-corporate FIIs. This led to panic selling by foreign investors. FIIs have offloaded equities worth over $3.2 billion since 5 July, destroying lakhs of crore of investor wealth since the budget announcement. The extent of damage has been so severe that even the renowned market experts have expressed it publicly that they have never witnessed so much wealth destruction in their entire career.

The risk appetite for equities is at its lowest. Looking at the pessimism on the street, there is a possibility that Indian markets may have already formed the bottom.

It is rightly said – ‘Bear markets sow the seeds of a new bull-run’. There is now a ray of hope as things seem to be turning around. On a positive note, the finance minister, who was not listening to the ground realities, has taken cognizance of the ongoing economic slowdown and has announced the much needed corrective steps to boost the economy. The surcharge on the super-rich was rolled back on capital gains.

The government has managed to get a whopping Rs1.76 lakh crore from the RBI in the form of dividend and transfer of reserves. This should provide relief to the government, which was struggling to maintain the fiscal balance due to lower tax revenues and uncertainty over divestment proceeds. This liquidity, along with the announcement of other measures, should boost the economy. In August, the RBI had announced an unconventional 35-bps rate cut. Inflation is expected to remain low with good monsoons and falling crude prices. There is scope for the RBI to cut interest rates further as India still has one of the highest real interest rates in the world.

While actual economic revival may take time, the markets usually start performing few quarters in advance. The current valuations are much below the long term average and hence deserve higher allocation to equities.The ongoing clean up by the government should help build a strong base for the new phase of growth.

This article is to be originally published in Business India Magazine.

Write to us at news@valuelineadvisors.com

Disclaimer: The views expressed in this article are personal and the author is not responsible in any manner for the use which might be made of the above information. None of the contents make any recommendation to buy, sell or hold any security and should not be construed as offering investment advice.