The decline in value of Japanese yen could open the floodgates of liquidity into the fast-growing emerging markets

A currency carry trade is a foreign exchange trading strategy, in which a currency trader sells a currency with relatively low interest rate and uses the funds to purchase a different currency yielding higher interest rates, in the bargain making some big bucks. The yen carry trade could be better explained as follows – a trader borrows Japanese yen from a Japanese bank and converts the funds into Indian rupee and buys Indian bonds for the equivalent amount. If we assume the bond pays 8 per cent and Japanese borrowing rate is 1 per cent, the trader stands to make a profit of 7 per cent, so long as the exchange rate between the countries does not change.

The yen carry trade can result in huge capital inflows into the currencies with high interest rates and capital outflows from the currencies with lower interest rates. This move results into strengthening of high interest rate currency against the lower interest rate currency. However, whenever these positions unwind, the effect on the currency also reverses automatically.

History shows that in the previous phase of bull-run during the last decade (between 2002 and 2007), one factors that fuelled it was the yen carry trade, where the investors borrowed money in Japanese Yen at lower interest rates and invested the borrowed money in different asset classes globally, which yielded higher returns. The yen carry trade is also considered to be one of the key factors that fuelled sub-prime crisis in the US.

Turn to the present decade. Japan, the world’s third largest economy, currently faces the problem of deteriorating fiscal position with public debt growing to 230 per cent of the GDP in 2011. This is coupled with the deflationary trend and negative GDP growth in the economy. In the second quarter of 2011-12, Japanese GDP contracted by a negative 0.5 per cent followed by further negative 0.9 per cent contraction in the subsequent quarter (third quarter of 2011-12). The contraction in the economy could be partly blamed on the continuously rising yen for the past many years, due to reversal of yen carry trade since the global meltdown of 2007 (post sub-prime crisis). The previous flush of liquidity due to yen carry trade had resulted in a massive bull run in various risk asset classes globally between 2002 and 2007.

As a damage control mechanism and to revive the ailing economy, the newly elected Japanese Prime Minister, Shinzo Abe, recently announced steps to boost the Japanese economy and tame the strong yen, which negatively affects Japanese exports. He has also set the medium term inflation target of 2 per cent from the current deflationary trend in the economy. The Japanese government has also recently approved ¥10.3 trillion ($117 billion) of fresh stimulus package to boost economic growth. The interest rates in Japan are amongst the lowest in the world at below 1 per cent.

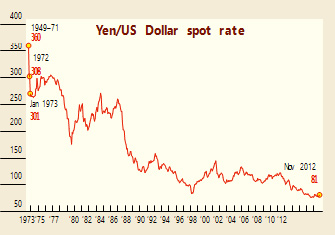

The worsening fiscal situation, expansionary monetary policy and low interest rates in Japan augurs for the weakening of Japanese yen, which could trigger a fresh round of yen carry trade. The Japanese yen has weakened over 17 per cent against the dollar, falling from the highs of 75.86 levels in October 2012 to 88.79 levels in January 2013, within the span of just three months.

Now, the weak yen could be used as a funding currency and is a bullish sign for the global equities and other risky asset class. The money moving out of the yen assets into high yielding risk assets globally could set a stage for the revival of fresh bull market, especially for the emerging economies like India, which have better growth prospects compared to the western world. Between January and November 2012 (a 11-month period), India has already seen FII inflows of over `1 lakh crore in Indian equities. As the Indian economic indicators look up, these inflows could only increase.

This article was originally published in Business India Magazine.

Write to us at news@valuelineadvisors.com

Disclaimer: The views expressed in this article are personal and the author is not responsible in any manner for the use which might be made of the above information. None of the contents make any recommendation to buy, sell or hold any security and should not be construed as offering investment advice.